DEVELOPER INCENTIVES BOLSTER NEW HOME SALES

The Power of Interest-Rate Buydowns in Today’s Higher-Rate Environment

New construction builders are gaining market share as existing home sales crawl to their slowest pace in decades. Since the majority of sellers are buyers, and most of them are less willing to let go of their lower-cost mortgages in exchange for higher-cost mortgages on potentially more expensive homes, the percentage of existing homes on the market has dwindled with the surge in interest rates.

In contrast, according to a new report from Redfin, the share of new construction homes available reached its highest share of any third quarter on record. Specifically, 30.6% of U.S. single-family homes for sale in the third quarter were new construction, up from 28.9% one year ago and 25% two years ago.

How are these builders winning in one of the least affordable housing markets ever recorded? Incentives. Unlike most existing home owners, home builders, especially institutional builders that construct homes at scale, have enough margin to offer compelling incentives to homebuyers, such as interest rate buydowns or closing cost credits. These incentives substantially reduce the initial cash required to close or, in the case of rate buydowns, have an outsized impact on a buyer’s monthly payment in comparison to a straight price cut. For example, a new construction development at Yerba Buena Island, The Bristol, is promoting a 5.5% rate buydown on its website, meaning buyers who purchase at the Bristol through an approved lender will have a 5.5% interest rate instead of something closer to the average 30-year-fixed rate today in the mid 7s. And the developer of a luxury building in San Francisco’s Cow Hollow neighborhood, Union House, offered a 3-2-1 buydown that would reduce the buyer’s interest rate by 3% in year 1, 2% in year 2, and 1% in year 3 before reverting to the prevailing rate in year 4.

These types of incentives are happening not just in the Bay Area, but all over the country, especially in communities dominated by large-scale development communities. According to an October survey conducted by the National Association of Home Builders, 62% of builders provided sales incentives (the majority of which were mortgage rate buydowns), while only 32% of builders reported cutting home prices. And its unlikely these incentives are going away any time soon, as its expected that interest rates will remain relatively elevated into 2024, and home builders have a continued need to move their product. Monthly supply of new homes sits at just under 8 months nationally, which favors buyers quite heavily, especially in comparison to the overall market, which sits at under half that. So institutional builders have relatively large volumes to sell and will continue to be creative to address buyers’ concerns in today’s market.

HAS THE MARKET REACHED ITS TROUGH?

Purchase Application Data on the Rise Following Drop in Rates

The average interest rate for 30-year fixed-rate mortgages jumped to over 8% in October, the highest level since November 2000, according to data from Freddie Mac. But after the Federal Reserve’s most recent meeting where it opted not to hike short-term borrowing rates again, at least for now, and weaker economic data reared its head, the average 30-year-fixed-mortgage rate fell to an average of 7.29% last week as the market became more optimistic that the Federal Reserve has finished its rate hiking campaign and might even start cutting short-term-borrowing rates by mid next year. Since the primary driver of the crash in homebuyer demand was the sharp increase in mortgage rates, you would expect to see an increase in homebuyer demand as interest rates ease. And that’s precisely what we’ve started to see since the October rate peak. As illustrated in the graph below which tracks purchase application (i.e., mortgage application) data along with mortgage rates, applications dip as rates rise, and applications rise as rates fall. And over the past 4 weeks since interest rates crested 8% and fell sharply into the low 7s, mortgage applications rose to their highest levels in weeks, and have steadily risen each of those 4 weeks.

If the market believes the Fed is done hiking, it could mean that we’ve reached the bottom of the existing home sales market from a transaction volume standpoint. Over history, when the Fed stops hiking rates, mortgage rates fall. And as we’ve seen, even slight downward moves for mortgage rates bring additional buyers to the market. And unless an outsized number of sellers who don’t intend to purchase another home start listing their homes, this also means buyer demand will outpace new supply, which leads to more buyers competing for existing inventory. This increase in demand, without a commensurate increase in supply, will keep prices elevated going forward.

How has the housing market remained so resilient from a price standpoint amid these mind-boggling statistics? Simple supply and demand. Inventory still remains constrained as most sellers don’t want to list their homes if it means exchanging cheap fixed mortgages for more expensive ones. And since life goes on (people downsize, people upsize, people get married, people get divorced), there is ample demand to keep up with supply and prevent prices from crashing and burning. If the Fed does respond with a firm statement at its next meeting at the end of this month and beginning of next month, expect to see sharp moves downward across the board--mortgage rates, Treasury yields, and rate/yield spreads. When exactly that will happen and whether those moves are enough to re-ignite buyer and seller demand, no one can say for sure. But expectations are that late this year / early next year will start to see some softening and volatility to calm down.

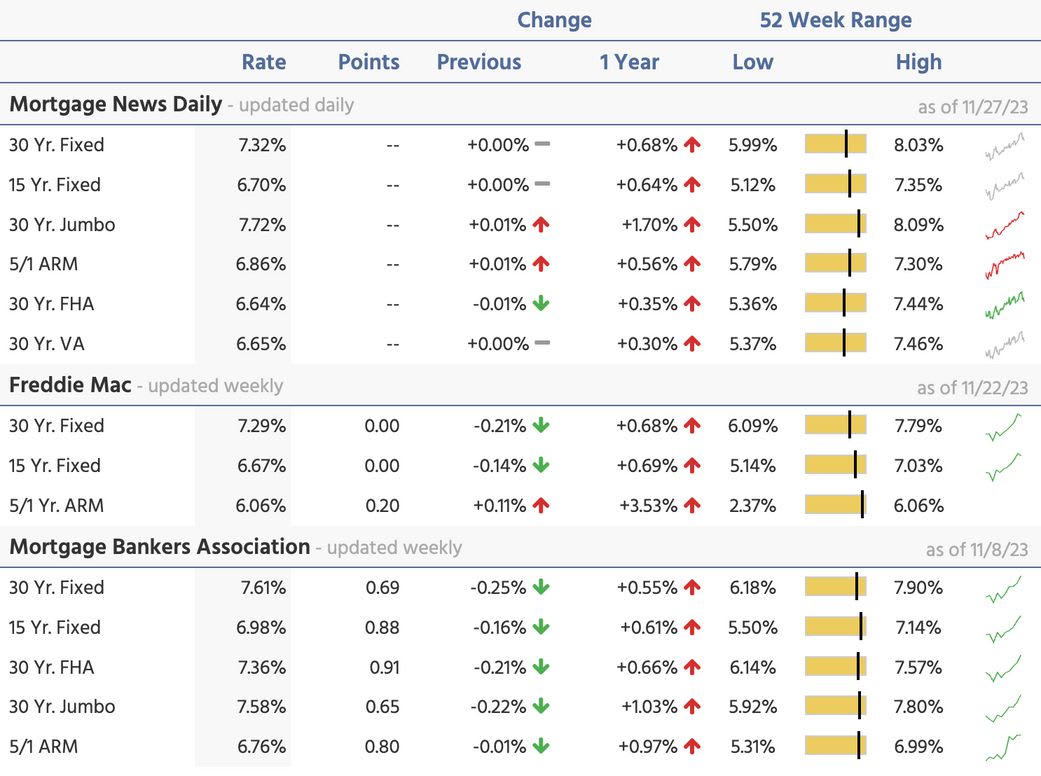

WHAT'S GOING ON WITH MORTGAGE RATES?

Rates Down Significantly Over Past Month Following Fed Pause

30-Year Fixed Mortgage Rate - One Year Trend