Demand slowdown, interest rate hikes, price-growth deceleration, price reductions, housing bubble, and recession. The headlines are painting pictures of doom and gloom in today's real estate market, but the data tells a different story.

Check out the latest housing statistics for San Francisco and Marin County, and read on to find out what's happening in today's national housing market and where experts predict the market is headed the second half of 2022.

The first half of 2022 was defined by rising interest rates, as the Fed aggressively increased rates, causing mortgage rates to increase from an average of 3% in January 2022 up to approximately 6% in an effort to fight inflation. Nationally, the rise in mortgage rates, combined with continuing price increases, has markedly increased the cost of ownership by an average of 64% year-over-year, tacking on over $800 / month to the cost of financing.

The main concern we hear today is that additional increases are going to bring on a recession (if we're not there already). If that happens, what does that mean for the housing market? Although the past is not always indicative of the future, there are trends we can learn from it. Throughout history, during recessionary period, interest rates tend to increase at the onset, and then decrease to re-stimulate the economy. Going back to the 1980s, interest rates drop an average of 1.8% from their peak seen during a recession to the trough, and in many cases continue to fall even after the recession is technically over.

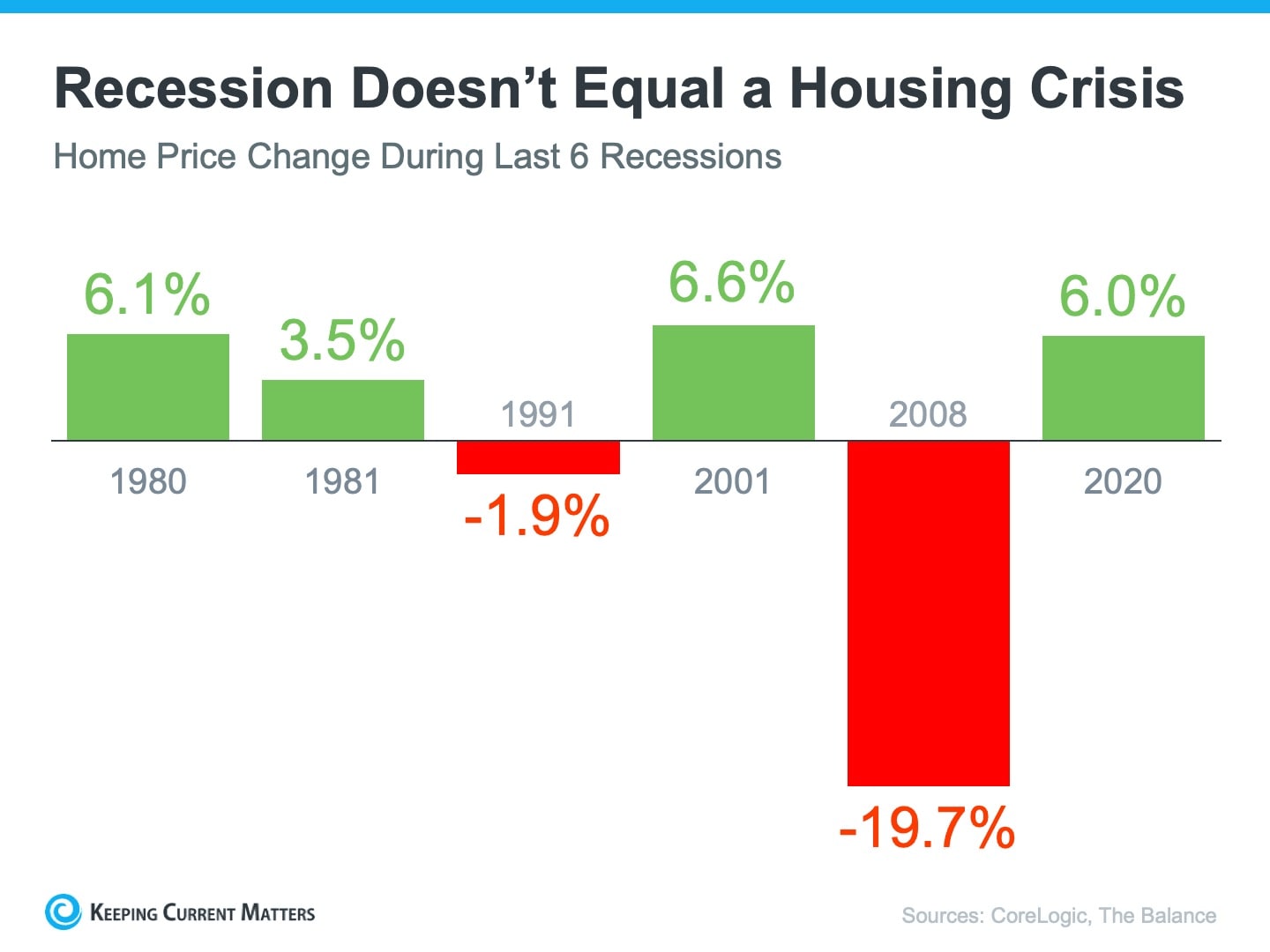

But what about prices? Since the 2008 Financial Crisis, the word "recession" has taken on new meaning. People hear that word and think about the disastrous impacts of that crisis on the housing market in particular. But, historically, recession doesn't necessarily mean housing crisis. In fact, during recessions dating back to the 1980s, housing prices (except during the 2008 financial crisis), have largely held stable or increased.

So, if recession doesn't necessarily mean home values drop, where are we going to end up in the second half of 2022 and going forward? While nobody has a crystal ball, the best way to answer that is by looking at market data and how it compares historically.

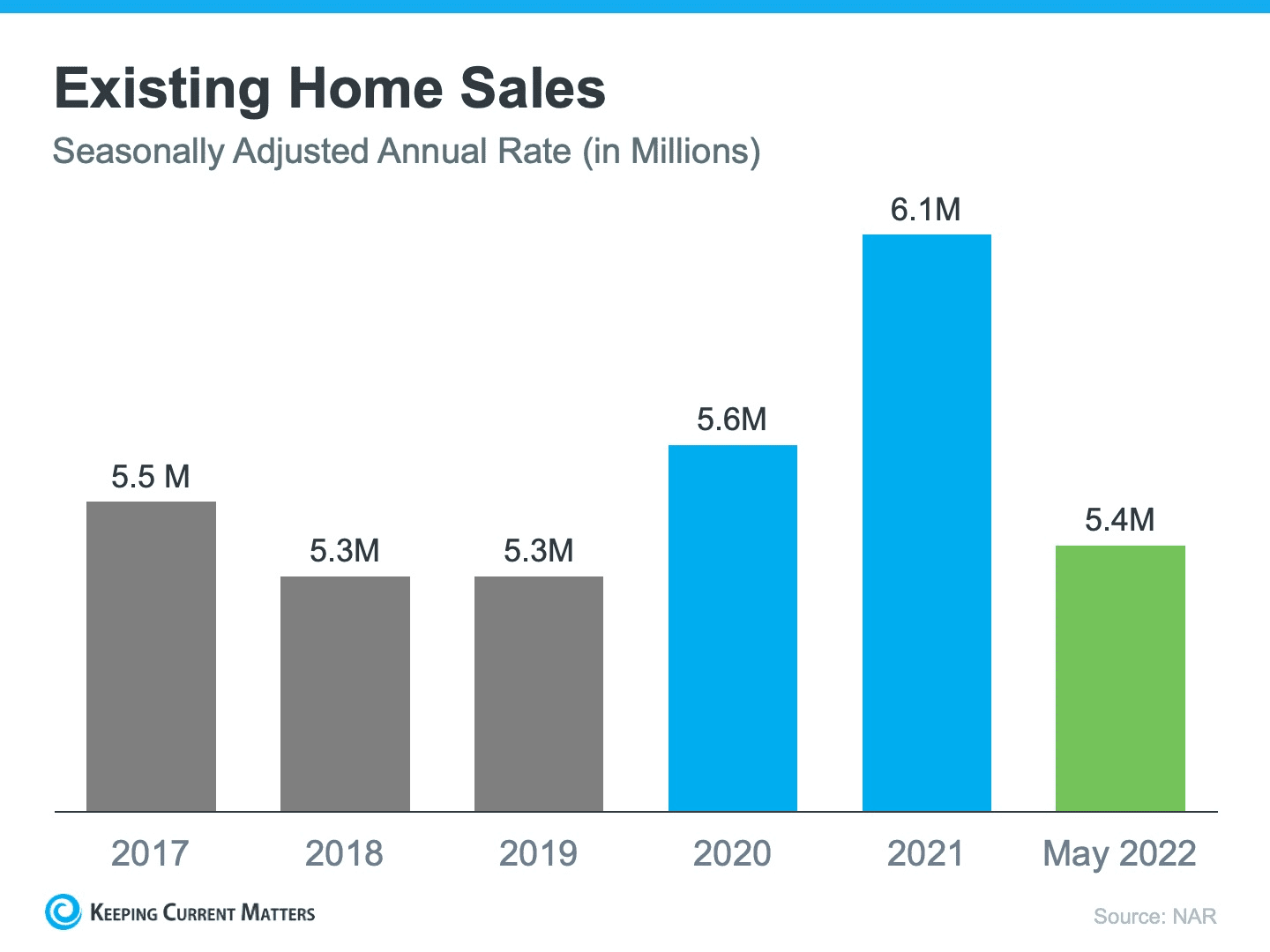

It's no surprise that increasing prices and mortgage rates have slowed demand for housing compared to the previous few months. But that demand, as measured by the number of showings and seasonally adjusted home sales, still exceeds pre-pandemic demand. Accordingly, while not at 2021's record-breaking levels, demand for housing remains comparatively stronger to levels of demand seen in previous years long-held to be strong years in the real estate market.

In addition to continued strong demand, the supply of housing remains relatively limited, further bolstering prices. For example, in San Francisco, monthly supply of single family homes (i.e., the time it would take to sell every home available assuming no new inventory came to market) is just 1.25 months, and in Marin County, 1.06 months. That means the number of single family homes available would need to at least triple, or demand for housing would need to fall at least by 66%, for the supply of housing to reach what is deemed a "neutral" market, typically 4-5 months of housing inventory available. And even more to reach "buyer's" market territory, typically 6-7 months of housing inventory available.

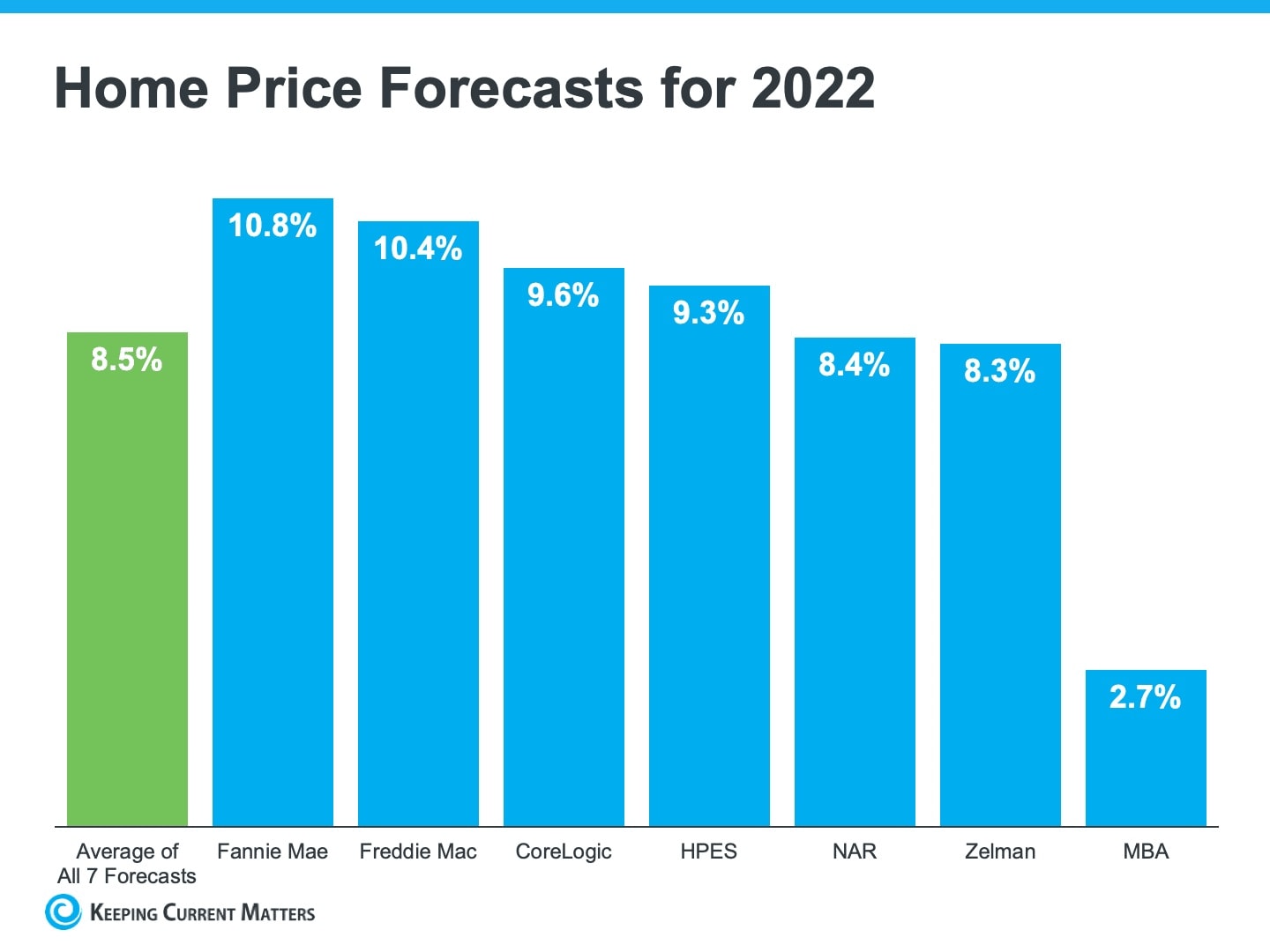

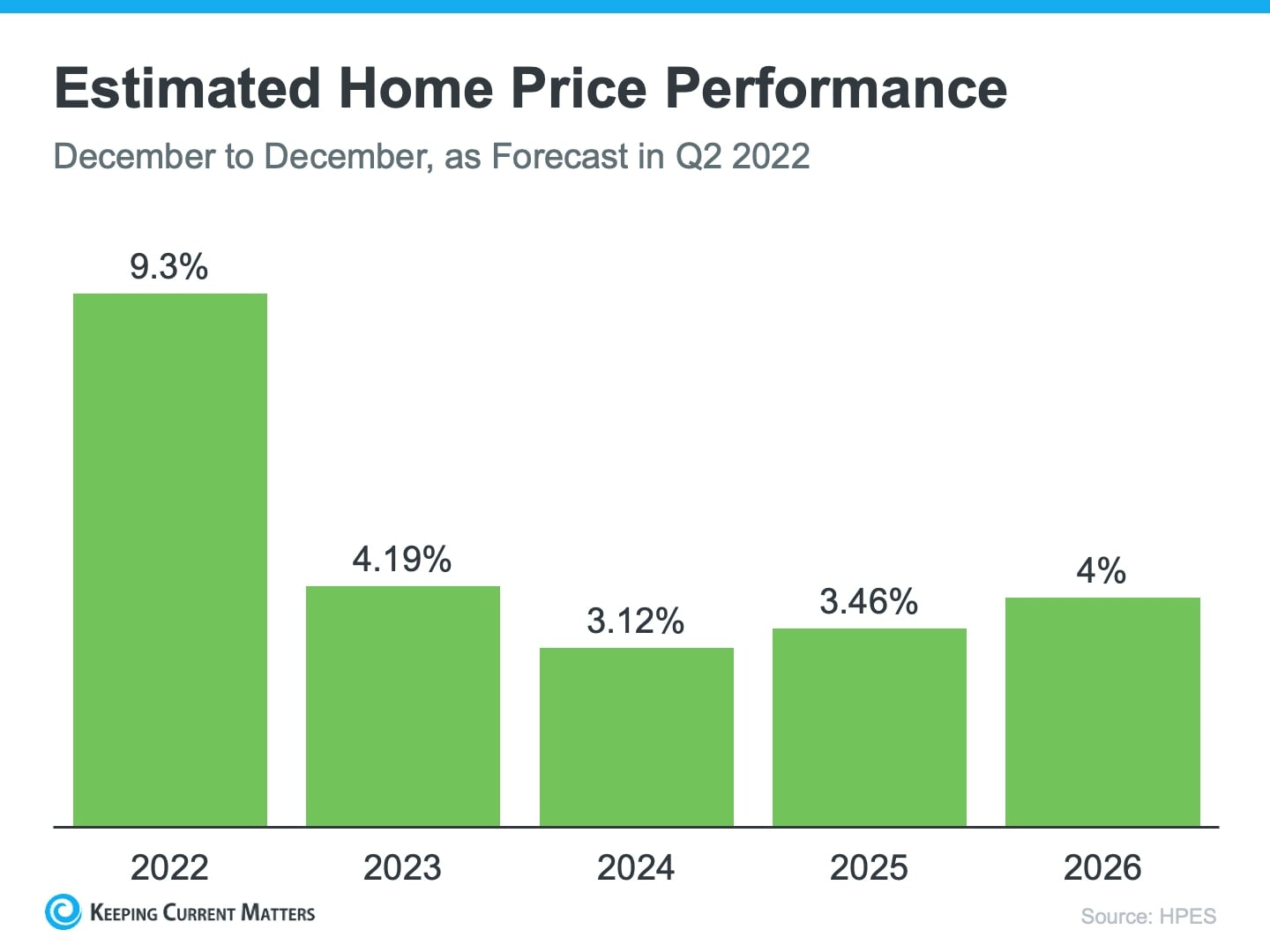

According to Realtor.com, "the nation is still suffering from a housing shortage that has reached crisis proportions at a time when many millennials are reaching the age when they start to consider homeownership. That’s likely to keep prices high." Indeed, experts predict housing prices will continue to rise this year by approximately 8.5%, and for the next several years between 3-4.2% each year. Is it the same 20%+ year-over-year growth we saw in 2021? No. That record-setting growth rate was unsustainable and nobody expected it would continue indefinitely. But just because home growth is slowing does not mean home value is depreciating. Deceleration does not equal depreciation.