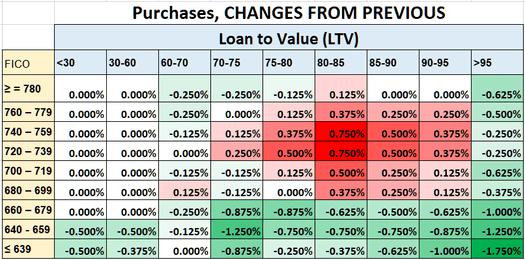

All of the sudden, social media and news outlets have people in a frenzy as reports surface about recent changes to loan level price adjustments (LLPAs) made by Fannie Mae and Fannie Mac to improve housing affordability. The changes, which take effect May 1, increase loan costs in certain instances for buyers with better credit, and decrease loan costs for buyers with worse credit. In some cases, the histrionics have gone so far as to suggest people are better off lowering their credit score to get a better deal. Not so fast.

LLPAs are, in fact, changing in a way that makes borrowing less expensive for buyers with lower credit scores and more expensive for those with higher credit scores. But people are confusing the change with the actual cost. As illustrated in the charts below, all other things equal, in no scenario will someone with worse credit pay less for their loan than someone with better credit. For instance, if you have a score of 640, you'll be paying significantly more than if you had a 740 credit score. Using an 80% loan-to-value ratio as an example, your LLPA at 640 is 2.25% versus 0.875% for a 740 score. So please don't purposefully ruin your credit immediately before applying for a mortgage.

Changes from Previous Pricing

Actual Differences

Builder Sentiment Continues Rise

Confidence up fourth month straight

The National Association of Home Builders (NAHB) / Wells Fargo's gauge of builder sentiment rose from 44 to 45 according to figures released April 17. Readings under 50 show a larger proportion of builders responding to the survey see market conditions as "poor" than those who see market conditions as "good."

So, while confidence has increased for the fourth month in a row, as mortgage rates and inflation have eased and inventory remains near historic lows, the measure still reflects general caution among builders, and is down significantly from 77 in April of last year.

Currently, one-third of housing inventory is new construction, compared to historical norms of a little more than 10%," according to NAHB Chief Economist Robert Dietz. He also noted that "more buyers looking at new homes, along with the use of sales incentives, have supported new home sales since the start of 2023. And while [Acquisition, Development & Construction] loan conditions are tight, there is not significant evidence thus far that pressure on the regional bank system has made this lending environment for builders and land developers worse.

While directionally positive, builders continue to see supply-chain challenges, especially with concrete and electrical transformer equipment, which has caused the price of those goods to increase and, in turn, bolster finished-product pricing

The sentiment index has three components: current sales, sales expectations, and buyer traffic. Current sales conditions rose 2 points to 51. Sales expectations in the next six months increased 3 points to 50, marking the first time both indicators were positive since June 2022. Buyer traffic was unchanged at 31, the first month it hasn't improved this year. Sales incentives by builders, including mortgage rate buy-downs, have boosted demand, and, consequently, the share of builders reducing home prices is still dropping. Just under a third of builders reported cuts in April, down from 35% at the end of last year, with an average reduction of 6%. Nationwide, reductions ticked down to 29.8% of homes as of last week, the highest on record for the week over the last five years, but down approximately 25% since the start of 2023.

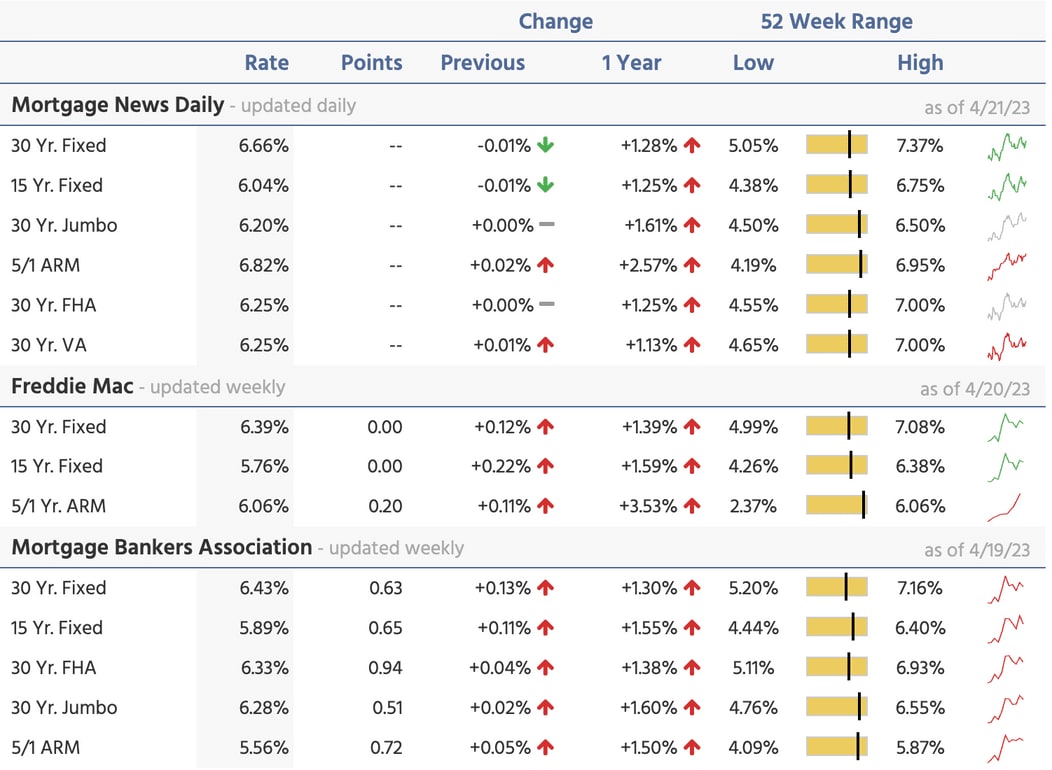

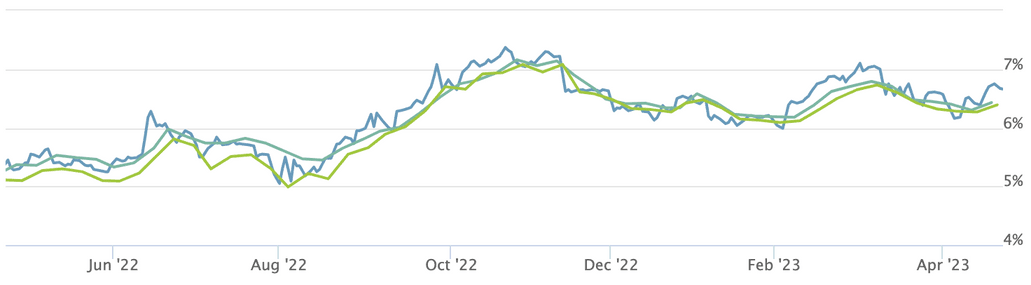

What's Going on With Mortgage Rates?

Rates tick up following strong economic data